Table of Contents

In 2017, J.P. Morgan introduced Chase Connect, an app for small and mid-sized companies, demonstrating its commitment to digital transformation in financial services. While a simple solution, it solved a key problem: 38% of startups fail due to cash flow problems.

This is just one example of the bank’s yearly commitment of $12 billion to technology.

J.P. Morgan’s focus on financial digital transformation is not unique. Research suggests that in 2023, global technology investments in banking and financial services was around $650 billion (roughly the size of Sweden’s GDP) and is growing at 9% a year on average. From banking-as-a-service (BaaS) to blockchain, digital transformation in financial services is hard to ignore.

In this blog post, we’ll explore what financial digital transformation involves, challenges it faces, and the benefits technology brings to finance.

What is Digital Transformation in Financial Services?

Digital transformation in financial services refers to the use of advanced technologies such as artificial intelligence (AI), cloud computing and data analytics, to find innovative solutions to market changes and customer demands.

For leaders, this means rethinking existing processes, breaking down data silos and focusing on more agile services.

Today, technology can improve operational efficiency, enhance customer experiences, and realize cost effectiveness. For instance, migrating to cloud infrastructure can save traditional banks up to 40% of costs through software and hardware savings, labor cost reduction, and even licensing spends.

In the long run, digitalization supports more personalized, responsive services, leading to stronger customer loyalty and higher lifetime value.

The Challenges to Financial Digital Transformation

Digital transformation in finance is reshaping the industry at an unprecedented rate, but it comes with unique challenges. From resistance to new technology to cybersecurity threats, roadblocks to financial digital transformation are plenty.

Yet, as we’ll see in a subsequent section, the benefits far outweigh the challenges. Before going into its advantages, let’s look at the challenges.

Digital upskilling and onboarding

Adopting financial technology requires employees to master new tools, which can create skill gaps and lead to resistance to change, making additional training necessary. Successful implementation of technology requires both technical training and cultural shifts within organizations.

In banks and financial institutions, this challenge is further compounded because of its high-stakes environment, where mistakes during the learning curve can lead to regulatory or financial risks.

Using a digital adoption platform (DAP) like Apty can help financial service companies provide employees with contextual as well as personalized AI-driven guidance, and customize their upskilling and onboarding processes to aid learning and cut costs.

Data privacy and cybersecurity

Digital transformation in financial services also comes with the threat of data breaches and cybersecurity attacks that threaten the privacy of sensitive information.

Recently, London-based Finastra that handles banking and wire transfers for more than 8,100 financial institutions globally, reported a major data breach impacting its internal file transfer system. This challenge can be prevented with robust encryption and security protocols, regular security audits, and AI-powered threat detection systems, among other solutions.

Integration with legacy software

Combining new digital tools with outdated systems can result in compatibility issues, ineffectiveness and high costs. A PYMNTS report found that 75% of banks struggle with digitalization because of legacy infrastructure. In fact, many banks in the Asia-Pacific continue to rely on decades-old legacy systems.

Instead of rapid digitalization, adopting a phased migration process that still retains critical infrastructure minimizes disruption, as has been seen in leading banks in countries like Australia and Singapore.

Real-time end user support

Complex digital systems can struggle to deliver fast solutions due to delays in troubleshooting, poor integration of customer data, or limited access to technical resources during crises.

For instance, a payment gateway crashing during a trading surge prevents users from executing trades. This results in huge financial losses for users and a damaged reputation for the financial intermediary.

Understanding end-user pain points

Failure to fully comprehend end-user needs can be frustrating for customers because of poorly designed or irrelevant digital solutions.

For example, providing customers with advanced cryptocurrency trades while having a user interface (UI) that is non-intuitive can result in low adoption rates. Companies like PayPal have overcome this through user journey mapping and A/B testing.

Cost of new technology

Advanced technologies such as AI or blockchain may require large upfront investments, ongoing maintenance costs and specialized expertise. These barriers can be prohibitive for smaller firms unless they explore cost-sharing models.

Regulatory compliance

As mentioned before, digital transformation in financial services requires compliance with many regulatory needs. For example, European Union (EU) banks and financial institutions that use AI must align with the GDPR, which has strict rules for data usage, storage and transparency.

Failure to comply with such guidelines can lead to hefty fines and legal repercussions, which can serve as a deterrent for many firms.

Benefits of Financial Services Digital Transformation

Despite its challenges, banks and financial institutions are moving towards digitalization. Players in the industry are recognizing the growing benefits of digital transformation for financial services, such as:

Enhanced customer experience

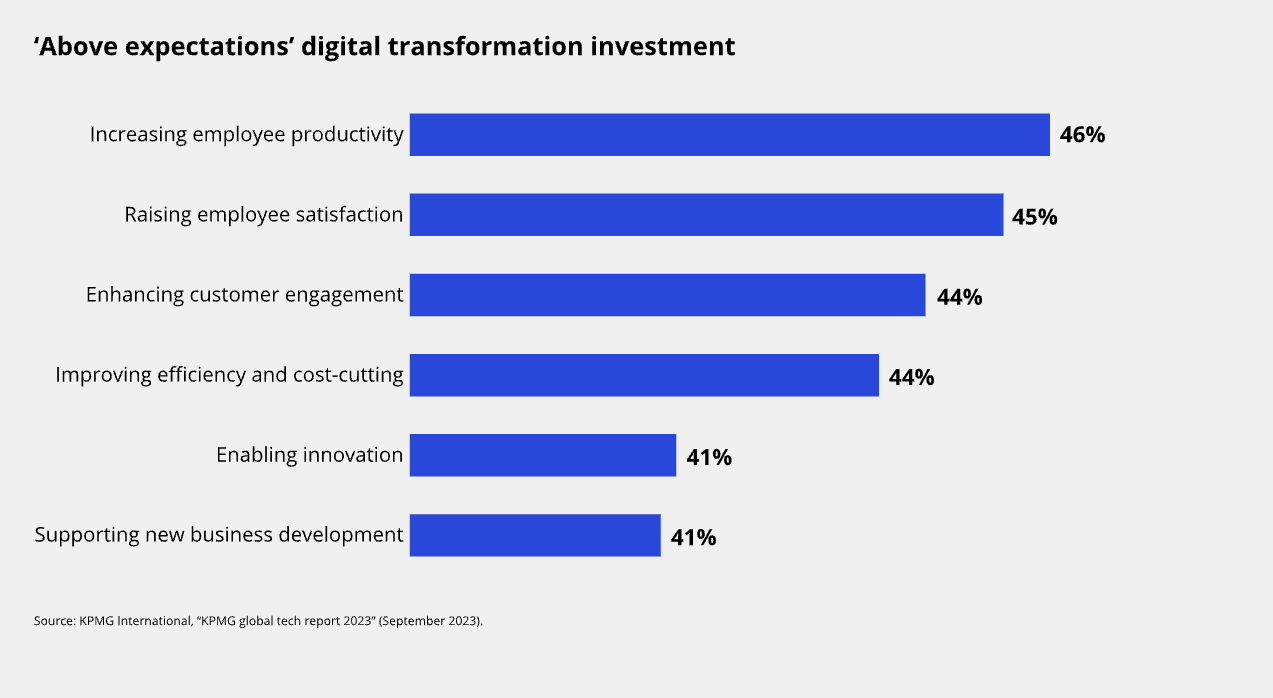

Digital transformation empowers financial institutions to deliver personalized, efficient, and consistent customer interactions. 44% of financial services executives reported enhanced customer engagement due to digital transformation investments.

For instance, implementing AI-powered chatbots and predictive analytics helps banks provide real-time customer support and tailored financial advice. Insurance company Lemonade’s AI bots Maya and Jim have made waves for their exceptional customer service and the company now has over 2 million customers.

Reduced operational costs

For financial institutions, automation and advanced digital software can streamline manual processes, ultimately cutting costs and enhancing efficiency. A KPMG report suggests that digital investments have already improved efficiency and supported cost benefits by 44% for financial services companies that have implemented them.

Easy data accessibility and management

Digital transformation for financial services can help collect, analyze, and store data, supporting decision-making with improved customer insights. Centralized platforms can integrate customer relationship management (CRM), transaction history, and third-party data, empowering internal teams with critical insights that can drive faster actions. Moreover, centralized data platforms can also support regulatory compliance through streamlined audits and data alignment with necessary standards.

Process agility and operational productivity

Software and new technology eliminate bottlenecks and combat human errors, which can improve process and operational agility. Machine learning solutions can streamline approvals, for instance, reducing processing time drastically.

The McKinsey Global Institute (MGI) estimates that across the global banking sector, gen AI could add between $200 billion and $340 billion in value annually, or 2.8% to 4.7% of total industry revenues, largely through increased productivity.

Examples of digital transformation in the finance industry

Financial digital transformation isn’t a new phenomenon, with many global companies leading the way. The benefits of digitization are best illustrated with real-life impact. Let’s explore real-world examples of digital transformation in the finance industry.

Digital customer onboarding

HSBC introduced SmartServe for digital onboarding by leveraging AI, machine learning and biometric verification. The impact of SmartServe has enhanced customer experiences where new accounts can be opened, information verified and KYC completed remotely and in real-time, within a few minutes.

At the same time, SmartServe has helped the bank expand into new markets and offer services to customers who may have previously found traditional banking procedures cumbersome.

Latest reports show that SmartServe is live in 19 countries, has more than 1,400 internal users and has onboarded 89% of eligible customers digitally, with 72% of them rating the experience as ‘easy’.

AI-driven fraud detection

Mastercard is paving the way for generative AI fraud detection to protect customers and payment networks. Its decision intelligence (DI) solution, launched earlier this year, scans one trillion data points in real time to detect the genuineness of transactions.

The existing AI technology already helps approve 143 billion transactions a year safely, while the new gen AI can boost fraud detection rates by up to 300%, based on initial modelling.

Robotic process automation

Robotic process automation (RPA) automates repetitive tasks, reducing errors and boosting employee productivity.

Deutsche Bank’s RPA commercialization program in China includes features like automated transaction data extraction and conversion from e-banking platforms, integration across multiple channels such as e-statements and e-wallets, and a zero human intervention reconciliation process. This has reduced reconciliation time from 2-3 days to under an hour. The pilot program shows that it can save the bank 60-80 hours of manpower per month.

CRMs for financial advisors

In 2023, Morgan Stanley took the leap into improving its CRM with an internal AI assistant powered by OpenAI’s ChatGPT technology.

AI @ Morgan Stanley Assistant changed how financial advisors and wealth managers handled client needs. It simplifies mundane tasks by quickly providing answers on investment or business performance from over 100,000 documents—much faster than human intervention. The assistant is seen as a “co-pilot” in the firm’s financial advisory department, with document access increasing from 20% to 80% and over 98% of advisor teams using it actively.

Banking-as-a-Service

The Apple Card, launched in partnership with Goldman Sachs, is a prime example of BaaS. It provides a digital-first banking experience seamlessly integrated within the Apple ecosystem.

While the card itself functions like a typical credit card, its backend infrastructure and financial services are powered by Goldman Sachs, using Apple’s advanced tech ecosystem to deliver a user-friendly, digital experience. Features include real-time transaction tracking, insights into spending habits and cash-back rewards.

Wealth management and Registered Investment Advisor platforms

Aladdin (Asset, Liability, Debt and Derivatives Investment Network) by BlackRock is a tech-powered investment management platform popular among financial institutions, asset managers, and institutional investors. It provides an impressive suite of tools for portfolio construction, risk management, trade execution, and performance analytics.

The system is preferred for its sophisticated risk analytics and ability to aggregate data from multiple sources into a unified view of portfolio performance. A key feature of Aladdin is its support for regulatory compliance, offering tools to help firms stay up-to-date with global regulatory changes.

Chatbots and virtual financial advisors

Going back to Lemonade’s example, the new-age insurer’s AI-driven chatbots, Maya and Jim, have significantly contributed to improved customer satisfaction and business performance.

Maya, the virtual assistant, processes insurance purchases and provides customers with instant quotes and responses. The company handles about 30% of customer interactions with absolutely no human intervention. Lemonade’s Jim handles claims processing and recently set a new record by settling a claim in two seconds.

The Apty Impact on Financial Digital Transformation

Modern software solutions are at the heart of digital transformation across industries. From workflow automations to data-driven analytics, digital tools set the stage for success. Enter Apty.io.

With contextual guidance and on-demand training, GenAI capabilities, integrations, and unified workspaces, Apty can accelerate your digital transformation in the finance industry. Apty’s DAP minimizes employee resistance and helps overcome change management challenges with a host of solutions that ensure successful adoption, including:

- in-app guidance to provide users with contextual support without interrupting their workflow

- AI-driven features offer role-based guidance, helping employees quickly master new tools and improve software utilization

- step-by-step guidance and process standardization to minimize errors and ensure that employees adhere to company procedures and compliance regulations

- analytics to track software usage patterns, providing organizations with data to optimize software utilization, manage licenses, and improve cost efficiency

Take the case study of this global bank in North America. It sought to improve the training and onboarding of its new project and portfolio management (PPM) software after a year of inefficiency and low productivity. The bank partnered with Apty for a solution.

Apty’s detailed guidance enabled employees to independently follow business processes, while real-time data validations and a predefined format for data entry improved accuracy and eliminated errors. The DAP’s analytics and reporting capabilities provided leadership with better visibility for key decision-making. As a result, the bank saved $1 million (80% of support costs) and reduced adoption time by 30 days.

Want these results for your own business? Join 12 million trusted Apty users on your digital transformation journey. Book a demo today!